How to Calculate Your Net Worth at 30 (Free Spreadsheet Template)

Net worth is the one number that shows you the real state of your finances — not your salary, not your savings account balance, but everything you own minus everything you owe. Here's how to calculate it properly, what the number actually means at 30, and what to do if it's negative.

Last updated: July 7, 2026 · 21 min read

The formula

That's it. Every financial complexity eventually reduces to this equation.

Most people in their 30s have a rough idea of their salary and maybe what's in their checking account. Very few have sat down and calculated their actual net worth — the full picture of where they stand after accounting for every asset and every debt.

That number matters more than your income. Someone earning $150k a year with $200k in student debt, a car loan, and no savings can have a lower net worth than someone earning $60k who's been quietly investing for eight years. Income flows through you; net worth is what stays.

This guide walks you through the full calculation, gives you a free spreadsheet template to do it yourself, explains what the result means at your age, and shows you the levers to pull if you want to change it.

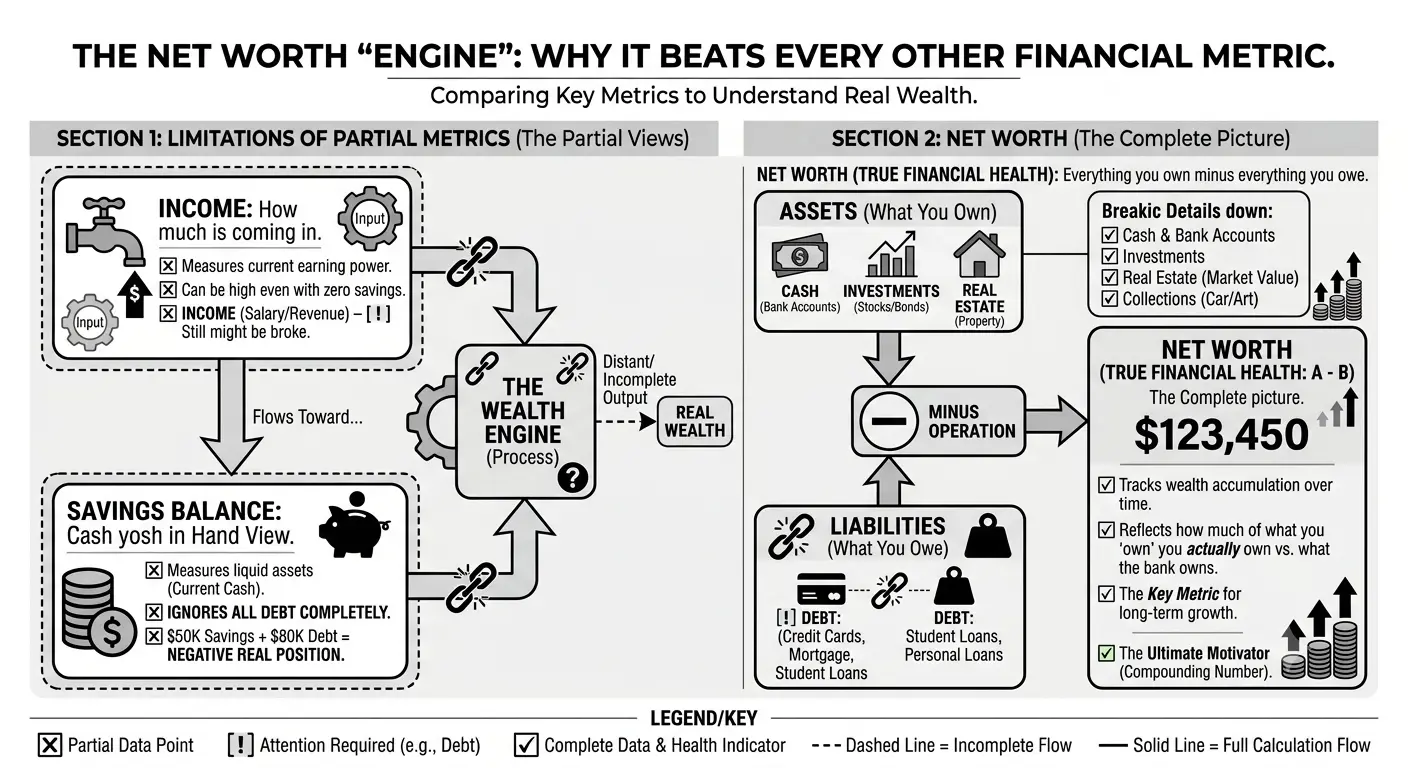

Why net worth beats every other financial metric

Income tells you how much is coming in. Your bank balance tells you how much you have right now. Net worth tells you how much you've actually kept — and how much of what you "own" you actually own versus what the bank owns.

Income

How much you earn

High earners can still be broke. Income without saving or investing builds no wealth.

Savings balance

Cash you have today

Ignores debts completely. $50k in savings + $80k in debt = negative real position.

Net Worth ✓

Everything you own minus everything you owe

The complete picture. Tracks wealth accumulation over time, not just cash flow.

Net worth also compounds as a motivator. Once you see the number, you want to watch it grow. It turns abstract financial goals ("save more money") into a single trackable number that moves visibly over time with the right habits.

Step 1 — List all your assets

An asset is anything you own that has monetary value. This sounds simple, but most people either miss things or overvalue things. Go through each category carefully.

💵 Cash & cash equivalents

Current balance- –Checking accounts

- –Savings accounts

- –Money market accounts

- –Cash on hand

- –CDs (certificates of deposit)

Use current balances. Easy to find — just log into your bank.

📈 Investment accounts

Current market value- –Brokerage accounts (stocks, ETFs, bonds, mutual funds)

- –Roth IRA

- –Traditional IRA

- –401(k) or 403(b)

- –HSA (Health Savings Account) invested balance

- –Crypto holdings

Use current market value for stocks and crypto — not what you paid.

🏠 Real estate

Estimated market value- –Primary home

- –Rental properties

- –Vacation property

- –Land

Use current market value, not purchase price. Check Zillow, Redfin, or a recent appraisal. Don't overestimate — be conservative.

🚗 Vehicles

KBB private party value- –Car(s)

- –Motorcycle

- –Boat, RV, trailer

Use Kelley Blue Book (KBB) private party value. Vehicles depreciate — their value is almost always less than you think.

💼 Other valuable assets

Conservative estimate- –Business ownership stake (use conservative estimate)

- –Vested stock options or RSUs

- –Life insurance cash value (not death benefit)

- –Valuables: jewelry, art, collectibles (if you'd actually sell them)

Be conservative and honest here. Only include things you could actually convert to cash.

⚠️ What NOT to count as an asset

Your future salary is not an asset. Your pension promise is debatable (include only if vested and you're very confident in it). Your parents' money is not yours. Personal belongings like furniture, electronics, and clothes technically have value but are not liquid and depreciate rapidly — most people leave them out for simplicity, which is fine.

Step 2 — List all your liabilities

A liability is anything you owe. This is where people often undercount — it's psychologically uncomfortable to add it all up, so they avoid it. Don't. The whole point of this exercise is to see reality clearly.

🏠 Mortgage(s)

Outstanding principal balance only — not the original loan amount.

Find it: Mortgage statement or lender online portal

🎓 Student loans

Federal + private, all of them. Include accrued interest if it's been capitalized.

Find it: StudentAid.gov for federal, lender portals for private

🚗 Auto loans

Remaining balance on any vehicle loans.

Find it: Lender statement or app

💳 Credit card balances

Current balance on each card — include any balance you carry month to month.

Find it: Each card's app or statement

🏥 Medical debt

Any outstanding medical bills or payment plans.

Find it: Bills or collection notices

👨👩👧 Personal loans

Loans from banks, credit unions, or individuals (including family).

Find it: Loan agreement or statement

📊 Other debt

Business loans you personally guaranteed, back taxes owed, legal judgments.

Find it: Tax records, legal documents

Step 3 — Calculate and interpret the number

Once you have both lists, the math is simple subtraction. Here's a worked example for a typical 30-year-old:

ASSETS

LIABILITIES

That's a positive net worth of $42,100. Is that good? Bad? Average? That depends — and we'll get to benchmarks in a moment. But the key thing is: now you know. This person earns their income, drives a car, carries student loans, and has been investing consistently. The number reflects all of that at once.

The free spreadsheet template (Google Sheets)

Rather than building this from scratch, use the template below. It's a Google Sheets file with all asset and liability categories pre-filled, automatic totals, and a simple chart that tracks your net worth over time as you update it monthly.

📊 Net Worth Tracker — Google Sheets Template

Free to copy and use. No sign-up required. Includes: all asset categories, all liability categories, automatic net worth calculation, monthly tracking rows, and a net worth growth chart.

✓ Pre-filled with all common asset and liability types

✓ Automatic =SUM() formulas — just fill in your numbers

✓ Monthly rows to track changes over time

✓ Automatic chart showing net worth trend

✓ Separate tabs for assets, liabilities, and history

Click "Make a copy" to save it to your own Google Drive. Your data stays private.

Build it yourself in 5 minutes

If you prefer Excel or want to build from scratch, here's the structure:

COLUMN A | COLUMN B

------------------|-----------

ASSETS |

Checking | [your value]

Savings | [your value]

Roth IRA | [your value]

401(k) | [your value]

Brokerage | [your value]

Home value | [your value]

Car (KBB) | [your value]

Other assets | [your value]

TOTAL ASSETS | =SUM(B2:B9)

|

LIABILITIES |

Mortgage | [your value]

Student loans | [your value]

Auto loan | [your value]

Credit cards | [your value]

Personal loans | [your value]

Other debt | [your value]

TOTAL LIABILITIES | =SUM(B12:B17)

|

NET WORTH | =B10-B18What's a good net worth at 30?

The most cited benchmark comes from the book The Millionaire Next Door, which suggests your net worth should be roughly your age multiplied by your gross annual income divided by 10. At 30 earning $70k, that would be 30 × $70,000 / 10 = $210,000.

That sounds like a lot — and for most 30-year-olds, it is. But it's worth knowing that this formula was designed for people further into their careers. For someone who graduated with debt and has been working for 5–8 years, a more realistic range is:

Below $0 (negative)

~30% of people in their late 20s / early 30s

Very common for people with student loans, especially recent grads or those who went to grad school. Not a crisis — but a signal to prioritize debt paydown.

$0 – $30,000

~20% of 30-year-olds

You have more than you owe. You're building — just slowly. Usually means you're carrying debt but have started investing.

$30,000 – $100,000

~25% of 30-year-olds

You're ahead of most peers. You've paid down meaningful debt, started investing, and built some cushion. This is the median range for 30-year-olds with stable careers.

$100,000 – $250,000

~15% of 30-year-olds

You've combined consistent investing, low debt, and likely a higher income or very disciplined spending. Top quartile for your age.

$250,000+

~10% of 30-year-olds

Usually a combination of high income (tech, finance, medicine), very early investing start, equity compensation (RSUs, options), or real estate appreciation. Top 10%.

Important context on benchmarks

These ranges vary enormously by location, career path, and life choices. Someone who bought a home in a city that appreciated 40% looks wealthy on paper but can't access that equity easily. Someone who paid off $80k in student loans has a far better trajectory than their net worth today suggests. The number matters less than the trend — is it going up every quarter?

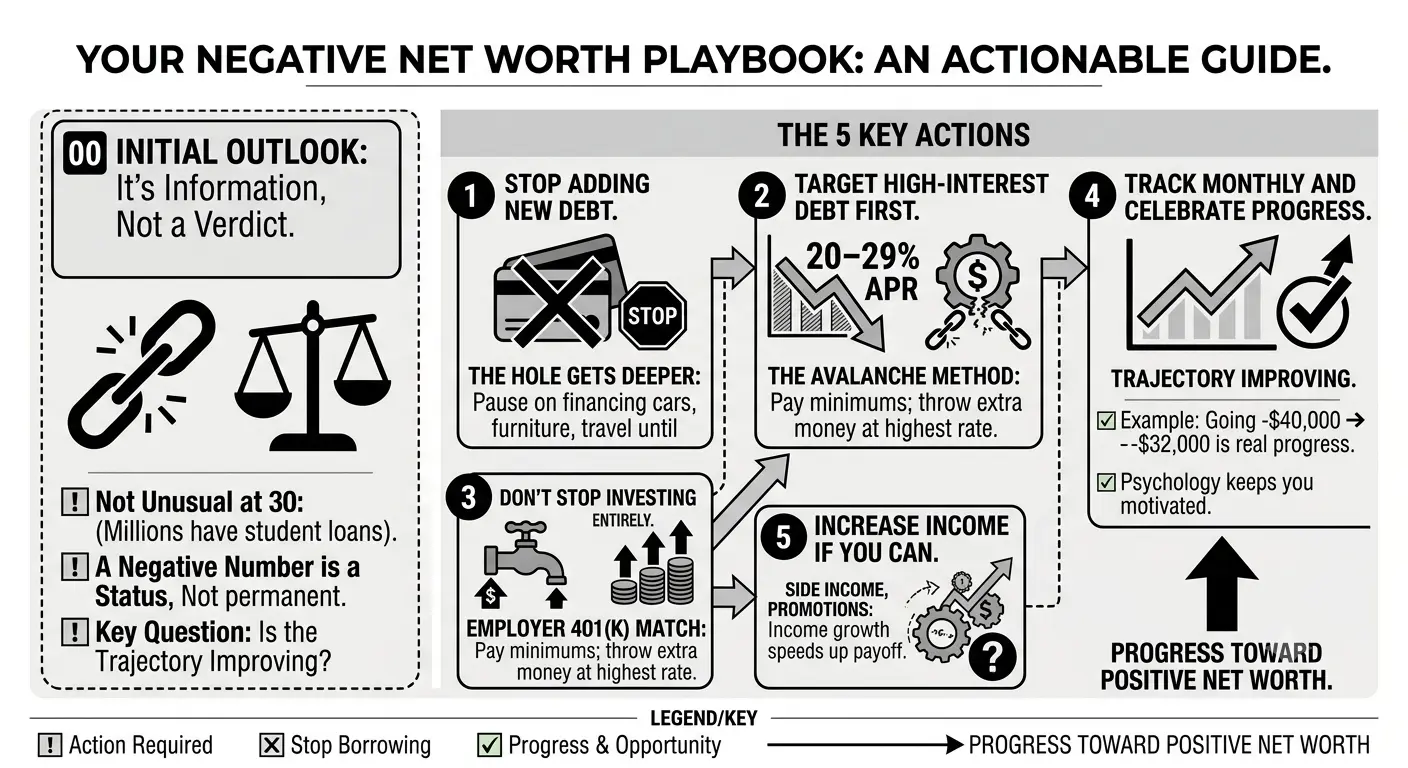

What if your net worth is negative?

First: this is not unusual at 30. Student loans alone push millions of people into negative net worth territory for years after graduation. A negative number is information, not a verdict.

What matters is whether the trajectory is improving. Here's what to do:

Stop adding new debt

The hole only gets deeper if you keep borrowing. Pause on financing anything new — cars, furniture, travel — until you've stabilized the balance sheet.

Target high-interest debt first

Credit card debt at 20–29% APR destroys net worth faster than almost anything else. Avalanche method: pay minimums on everything, throw every extra dollar at the highest-rate debt.

Don't stop investing entirely

If your employer offers a 401(k) match, contribute at least enough to get the full match — that's a guaranteed 50–100% return. Beyond that, prioritize high-interest debt over investing.

Track monthly and celebrate progress

Going from -$40,000 to -$32,000 is real progress. Update your spreadsheet monthly. The psychological effect of watching the number improve keeps you motivated.

Increase income if you can

At a negative net worth, income growth has outsized impact. A $10k salary increase applied to debt payoff can cut years off your timeline. Side income, promotions, career moves — all accelerate the climb.

How to grow your net worth in your 30s

Your 30s are the most important decade for building wealth. The decisions you make between 30 and 40 compound more powerfully than any other decade — there's enough time ahead for investments to grow, but also enough working years left to meaningfully increase income.

Maximize retirement accounts

High impact401(k) limit is $23,000/year in 2026. Roth IRA is $7,000. Max both if possible. Tax-advantaged growth is the highest-return move available to most people.

Invest in low-cost index funds

High impactS&P 500 index funds have averaged ~10% annually over decades. Stop trying to pick stocks. VTSAX, VTI, or your 401(k)'s equivalent are the right default.

Pay down high-interest debt aggressively

High impactPaying off a 22% credit card is a guaranteed 22% return. Nothing in the stock market comes close to that risk-adjusted.

Avoid lifestyle inflation

Medium impactEvery raise you get is an opportunity to either increase savings rate or increase spending. The people who build wealth fastest bank the raise and keep living on the previous income.

Build marketable skills

High impactYour income is your biggest asset before 40. A $15k/year raise invested over 10 years is worth more than almost any other financial move.

Automate everything

Medium impactSet up automatic transfers to savings and investment accounts the day your paycheck hits. Money you never see in checking gets invested. Money that sits there gets spent.

How often should you recalculate?

Once a month is the sweet spot for most people. It's frequent enough to see the trend clearly, but not so frequent that market fluctuations make it feel like a rollercoaster.

Pick a specific day — the first of the month is easy to remember — log into your accounts, update the spreadsheet, and you're done. The whole process takes about 10 minutes once the template is set up.

Suggested update schedule

FAQ

Should I include my car as an asset?↓

Do I include my 401(k) in net worth even if I can't touch it until 59½?↓

My home is worth more than when I bought it. Should I use the current value?↓

Should I include my spouse or partner's assets and debts?↓

I have stock options that haven't vested yet. Do they count?↓

My net worth went down this month because the stock market dropped. Is that normal?↓

Quick recap

- 1Net worth = Total Assets − Total Liabilities. The only number that shows your full financial picture.

- 2List every asset at current market value — cash, investments, retirement accounts, home, car.

- 3List every liability at current balance — mortgage, student loans, car loans, credit cards.

- 4A negative net worth at 30 is common, especially with student debt. Track the trend, not just the number.

- 5The median 30-year-old has a net worth between $30k–$100k. But context matters more than comparisons.

- 6Use the free Google Sheets template and update it on the 1st of every month.

- 7The biggest levers: max retirement accounts, pay off high-interest debt, avoid lifestyle inflation, grow income.

Next steps

Now that you know your net worth, these guides help you grow it: