ETF Investing Fundamentals

Exchange-Traded Funds have become the default building block for millions of long-term investors — and for good reason. This guide explains exactly how they work, what makes them so cost-effective, and how to use them to build a portfolio that doesn't require constant attention.

By the numbers

⚠️ For educational purposes only

What Is an ETF?

An Exchange-Traded Fund is exactly what its name says: a fund you can buy and sell on a stock exchange, just like a share in any individual company. What makes it a fund is that it holds a collection of assets — typically stocks, bonds, or commodities — rather than representing ownership in a single business.

When you buy one share of a broad-market ETF like VTI (Vanguard Total Stock Market ETF), you're instantly invested in roughly 3,700 US companies — from Apple and Microsoft down to small regional businesses — in a single transaction. That kind of instant diversification used to require either a large amount of capital or a mutual fund with high minimum investments.

The "exchange-traded" part is what sets ETFs apart from traditional mutual funds: they trade continuously throughout the day at market prices, not just once at the end of the day. This gives investors far more flexibility in when and how they buy and sell.

How an ETF is structured

You buy

ETF shares on an exchange

ETF holds

a basket of assets

Assets include

stocks, bonds, commodities…

You own

a proportional slice

ETFs vs. Mutual Funds

Both ETFs and mutual funds pool money from many investors to buy a collection of assets. But there are meaningful differences in how they're structured, priced, and taxed — and those differences matter over the long run.

| Feature | ETF | Mutual Fund |

|---|---|---|

| Trading | Throughout the day at market price | Once daily at NAV after market close |

| Minimum investment | Price of one share (often <$10) | Often $500–$3,000+ |

| Expense ratios | Very low (0.03%–0.20% typical) | Higher (0.50%–1.50% active funds) |

| Tax efficiency | High — rarely distribute capital gains | Lower — capital gains often distributed |

| Transparency | Holdings disclosed daily | Holdings disclosed quarterly |

| Automatic investing | Requires a broker with fractional shares | Often built-in via fund company |

💡 The index fund connection

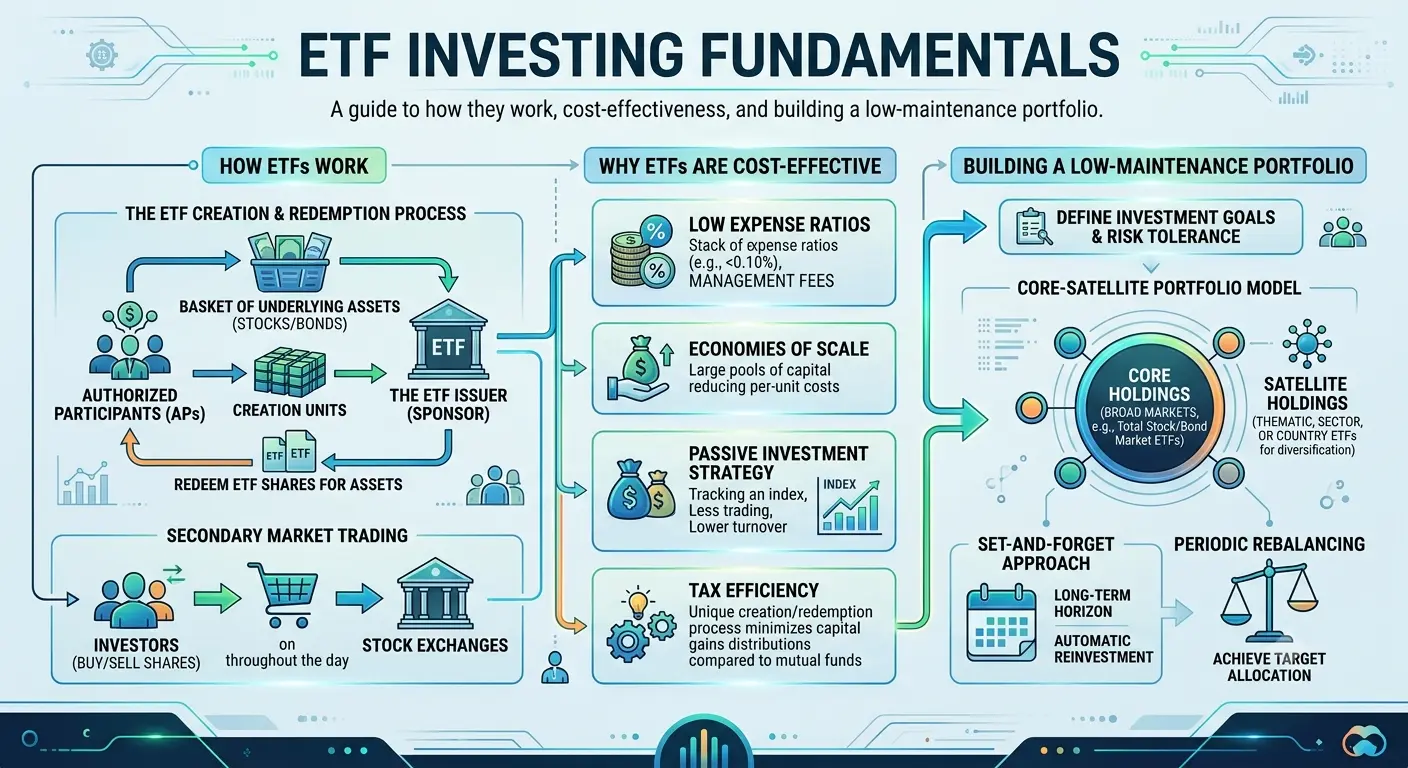

How ETFs Trade

Understanding a few mechanics makes you a better ETF buyer — particularly when it comes to getting a fair price.

Market price vs. NAV

An ETF's Net Asset Value (NAV) is the total value of all the assets it holds, divided by the number of shares outstanding — updated once daily. But because ETFs trade on exchanges throughout the day, the actual market price can differ slightly from NAV. This difference is called the premium (when price exceeds NAV) or discount (when price is below NAV).

For large, liquid ETFs tracking major indices, premiums and discounts are typically tiny — fractions of a percent — because large financial institutions called authorized participants can create or redeem ETF shares at NAV, keeping the price in line. For small, illiquid ETFs, the gap can be larger and worth watching.

The bid-ask spread

Every ETF has a bid price (what buyers will pay) and an ask price (what sellers want). The difference — the spread — is a transaction cost you pay on every trade. For a popular ETF like SPY (one of the most traded securities in the world), this spread is less than a cent. For thinly traded niche ETFs, it can be a meaningful cost.

Use limit orders, not market orders

When buying ETFs, use a limit order rather than a market order. A limit order lets you set the maximum price you're willing to pay — your order only executes at that price or better. A market order executes immediately at whatever the current ask price is, which can work against you during periods of high volatility or low liquidity. The extra ten seconds to set a limit is almost always worth it.

Types of ETFs

Broad market

Most popularVTI / VWRATrack an entire market — US or global. The workhorse of most long-term portfolios. Maximum diversification at minimal cost.

Sector

Concentrated riskXLK / XLEFocus on a specific sector like technology, energy, or healthcare. Useful for targeted exposure, but inherently less diversified.

Bond / Fixed income

Lower volatilityAGG / BNDHold a basket of bonds — government, corporate, or both. Used to balance equity risk in a portfolio as investors approach their goals.

International

Diversifies geographyVXUS / EEMProvide exposure to markets outside your home country — developed markets, emerging markets, or both. Essential for true global diversification.

Dividend

Income focusVYM / SCHDFocus on companies with a history of paying dividends. Popular among income-oriented investors, though total return matters more than yield alone.

Thematic

SpeculativeARKK / ICLNTrack a specific investment theme — clean energy, AI, genomics. Higher potential, higher risk, and often higher expense ratios. Approach with care.

Key Metrics to Evaluate Before You Buy

Not all ETFs tracking the same index are equal. Here's what to check before committing to any specific fund.

Expense Ratio (ER)

What it is

The annual fee deducted from fund assets, expressed as a percentage.

Why it matters

A 0.50% ER vs. 0.05% ER costs you $45 per year on every $10,000 invested — small amounts that compound into significant differences over decades. Always choose the cheapest fund tracking an index you want, all else being equal.

📊 Target: below 0.20% for broad market, below 0.50% for specialist

Assets Under Management (AUM)

What it is

The total value of all assets held by the ETF.

Why it matters

Larger AUM generally means tighter bid-ask spreads, lower tracking error, and less risk the fund is closed before you want to sell. As a rough guide, avoid ETFs with less than $100M in AUM.

📊 Target: $500M+ preferred, $100M+ acceptable

Tracking Error

What it is

How closely the ETF follows its target index's returns.

Why it matters

A well-run ETF should return almost exactly what its index returns, minus its expense ratio. Large tracking errors suggest the fund is managing its portfolio poorly. Most major ETFs from Vanguard, BlackRock (iShares), and State Street (SPDR) have near-zero tracking error.

📊 Target: as close to 0% as possible

Trading Volume

What it is

The average number of shares traded per day.

Why it matters

High volume = tight spreads and easy execution. Low volume can mean wider spreads, making it more expensive to buy and sell — a hidden cost that doesn't appear in the expense ratio.

📊 Target: consistent daily volume across market conditions

Dividend Yield & Distribution

What it is

How much income the fund distributes, and how often.

Why it matters

Relevant if you want income from your investments. Also affects your tax situation: ETFs distributing dividends create a taxable event each time, even if you reinvest. In tax-advantaged accounts, this doesn't matter.

📊 Depends on your income vs. growth goals

Building a Portfolio with ETFs

One of the most important lessons from decades of investing research: you don't need a complicated portfolio. A simple, low-cost, diversified allocation beats most sophisticated strategies — especially after fees and taxes.

The three-fund portfolio

Probably the most recommended starting point for long-term investors worldwide. Three ETFs, globally diversified, cheap to run, and easy to rebalance once a year:

US stocks

VTICore growth engine

e.g. 60%

International stocks

VXUSGeographic diversification

e.g. 30%

Bonds

BNDStability & ballast

e.g. 10%

🎯 Asset allocation is personal

Rebalancing: the discipline that matters most

Over time, your allocations will drift as different assets grow at different rates. If you set a 60/30/10 target but equities surge, you might drift to 75/20/5 — taking on more risk than you intended. Rebalancing means selling what has grown above your target and buying what has fallen below it, returning to your target allocation.

Once or twice a year is sufficient for most investors. In tax-advantaged accounts, rebalance freely. In taxable accounts, try to rebalance using new contributions first to minimize taxable events.

Tax Efficiency of ETFs

One of ETFs' most underappreciated advantages is their structural tax efficiency — and it comes from a mechanism most investors never think about.

When mutual fund investors sell shares, the fund manager has to sell underlying assets to raise cash — creating capital gains that are distributed to all shareholders, even those who didn't sell. You can owe taxes on gains you never personally realized.

ETFs avoid this through the in-kind creation/redemption mechanism: authorized participants exchange baskets of the underlying stocks for ETF shares (or vice versa) without triggering a sale at the fund level. The result is that ETFs rarely distribute capital gains to shareholders, making them far more tax-efficient in taxable accounts.

✅ Best for taxable accounts

🏦 Account location matters

Common ETF Investing Mistakes

✗ Chasing recent performance

An ETF that returned 40% last year is not necessarily a better investment than one that returned 10%. Sector ETFs often top performance charts in the year they peak — right before they fall. Base decisions on fundamentals, not recent returns.

✗ Over-diversifying with too many ETFs

Holding 15 ETFs doesn't mean you're 15× more diversified than holding 3. If those 15 ETFs all hold large US tech stocks, you have significant overlap and far more complexity than benefit. More funds ≠ more diversification.

✗ Ignoring total costs

The expense ratio is only one cost. Factor in: trading commissions (though most major brokers now offer commission-free ETF trading), bid-ask spreads, and currency conversion fees for international ETFs.

✗ Treating leveraged or inverse ETFs as long-term holds

Leveraged ETFs (2× or 3× daily returns) and inverse ETFs are designed for short-term trading, not long-term investing. Due to volatility decay, they reliably underperform their stated multiplier over longer periods — often dramatically.

✗ Panic-selling during market downturns

The biggest threat to your long-term returns isn't market volatility — it's your own reaction to it. Selling a broad index ETF during a downturn locks in losses and typically means missing the recovery. Time in the market beats timing the market.

How to Get Started

The mechanics of buying your first ETF are simpler than most beginners expect. Here's the path from zero to first purchase.

Open a brokerage account

Choose a reputable, low-cost broker — Fidelity, Charles Schwab, and Vanguard in the US; Interactive Brokers, Trading 212, or your bank's investment arm internationally. Look for zero commission on ETF trades and fractional share support.

Choose a tax-advantaged account type first

Before investing in a taxable brokerage account, max out any available tax-advantaged accounts: 401(k), IRA, Roth IRA (US); ISA (UK); RRSP, TFSA (Canada). The tax savings compound just like investment returns.

Decide on an asset allocation

Based on your time horizon and risk tolerance, decide your target split between equities and bonds. If you're more than 20 years from needing the money, a heavy equity allocation (80–100%) is commonly recommended by financial planning research.

Select your ETFs

Start simple. A single global ETF (like Vanguard's VWRA or iShares' IWDA + EMIM) gives you exposure to thousands of companies worldwide at very low cost. You can add complexity later; it's much harder to simplify an overly complex portfolio.

Set up automatic contributions

Dollar-cost averaging — investing a fixed amount on a regular schedule regardless of market conditions — removes the psychological burden of timing the market and steadily builds your position over time. Most brokers support automated recurring investments.

ETF Investor Checklist

Before and after making any ETF investment, run through these:

Before you buy

- Checked the expense ratio (aim for <0.20%)

- Verified AUM is above $100M

- Confirmed low tracking error vs. benchmark

- Reviewed holdings to check for overlap with existing funds

- Used a limit order, not a market order

Portfolio health

- Overall allocation matches my risk tolerance

- No single sector or country dominates

- Bond/equity ratio appropriate for my timeline

- Scheduled annual rebalance date

- High-income ETFs in tax-advantaged accounts

Ongoing habits

- Automatic contributions set up

- Not checking portfolio more than monthly

- Reinvesting dividends automatically

- Not reacting to short-term market moves

- Expense ratios reviewed if new alternatives launch

Avoid these

- Leveraged or inverse ETFs for long-term holding

- ETFs with <$50M AUM

- Chasing last year's top-performing sector

- Paying >0.75% ER for a passive index ETF

- Panic selling during market corrections

The bottom line

Simple, low-cost, and consistent.

That's the entire strategy.

The evidence is remarkably clear: a handful of broad index ETFs, held for the long term with regular contributions and minimal tinkering, outperforms the vast majority of complicated strategies. The hardest part isn't the analysis — it's the patience.

Finance & Fintech Research Team

The Kodivio team analyzes financial tools, investment platforms, and fintech trends based on independent research and market data.

Learn more about us →