Dividend Investing for Beginners: How to Earn Monthly Passive Income

A practical, beginner-friendly guide to dividend investing: how dividends work, how to build a monthly income portfolio, the metrics that actually matter, and the mistakes that trip up new investors.

Somewhere between a savings account and a full-blown trading habit sits one of the most underrated ways to build wealth: owning companies that pay you simply for holding their stock. That's the whole idea behind dividend investing, and it's a strategy that has quietly funded retirements, college tuition, and mortgage payments for generations of ordinary investors.

If you've ever wondered how some people seem to collect a check every month without touching their investments, this guide breaks down exactly how it works — from the mechanics of a dividend payment to building a portfolio that pays you on a rolling monthly schedule.

What Is Dividend Investing, Exactly?

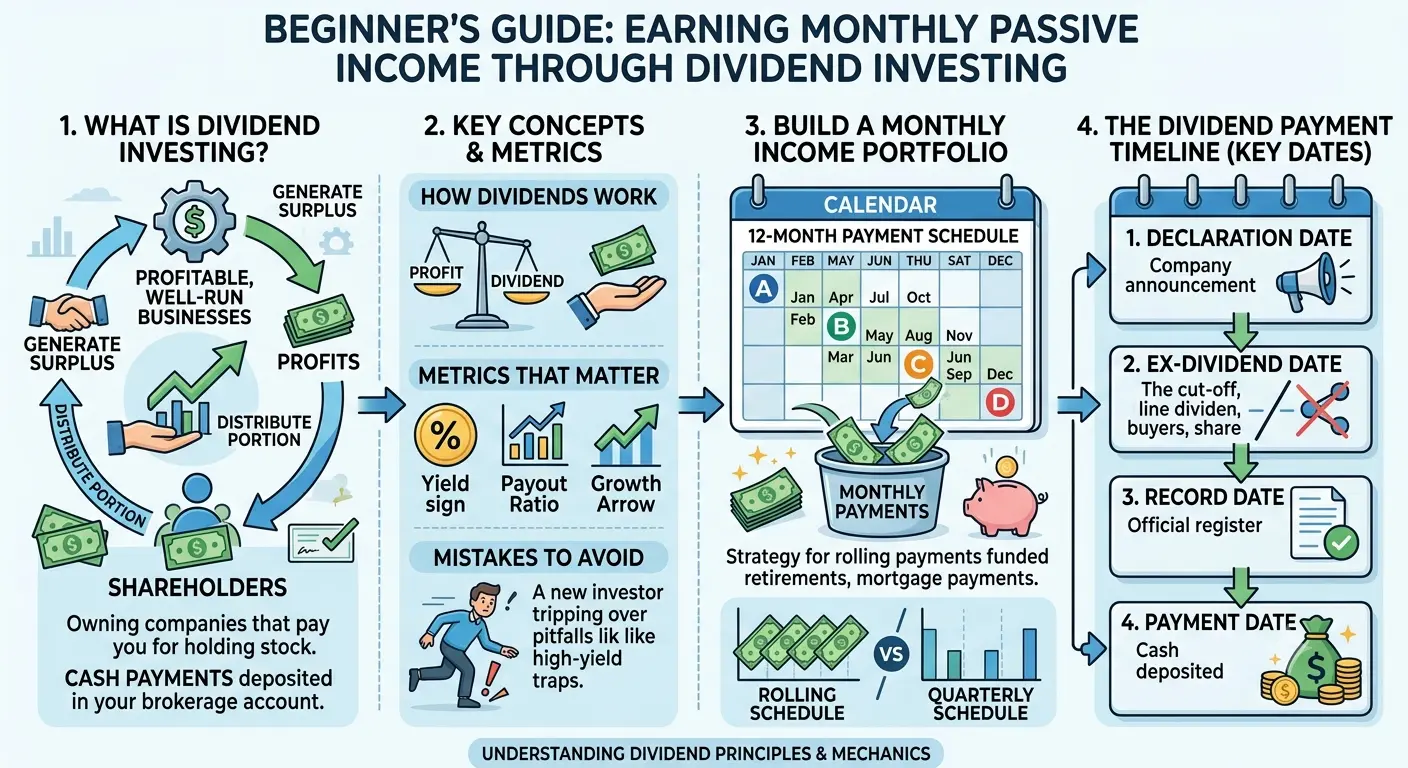

Dividend investing means buying shares of companies that distribute a portion of their profits back to shareholders on a regular basis, instead of (or in addition to) reinvesting every dollar into growth. When you own even one share of a dividend-paying company, you're legally entitled to your slice of that payout — typically deposited straight into your brokerage account in cash.

It's a strategy built on a simple premise: profitable, well-run businesses often generate more cash than they need to reinvest in operations, so they share the surplus with the people who own them. Over time, that steady stream of payments can become a genuine source of passive income.

How Dividends Actually Work

Before you can build a dividend strategy, it helps to understand the timeline behind every payment. Companies don't just send out cash randomly — the process follows four key dates.

| Date | What It Means |

|---|---|

| Declaration Date | The company's board officially announces the dividend amount and schedule. |

| Ex-Dividend Date | You must own the stock before this date to qualify for the upcoming payment. |

| Record Date | The company checks its books to confirm who officially owns shares. |

| Payment Date | Cash actually lands in your brokerage account. |

The detail most beginners miss is the ex-dividend date. Buy a share even one day after it, and you'll miss that round of payments entirely — you'll have to wait for the next cycle.

Why Investors Turn to Dividend Stocks for Passive Income

Dividend investing appeals to a wide range of people, but a few reasons come up again and again:

- Cash flow without selling assets. You get paid while still owning the underlying investment, rather than having to sell shares to generate income.

- A signal of financial health. Companies that pay consistent dividends are often profitable, disciplined, and confident enough in future earnings to commit to regular payouts.

- Compounding through reinvestment. Reinvested dividends buy more shares, which then generate their own dividends — a snowball effect that accelerates over decades.

- A cushion during downturns. Dividend payments can soften the emotional and financial impact of a falling stock price, since you're still collecting income even if share value dips temporarily.

Building a Monthly Dividend Income Portfolio

Here's the part most beginners find surprising: the majority of individual dividend stocks pay quarterly, not monthly. So how do people end up with a check landing in their account every single month? The trick is staggering.

By combining companies that pay on different quarterly schedules — or mixing in a handful of stocks and funds that pay monthly by design (common in real estate investment trusts, or REITs) — you can build a portfolio where at least one payment arrives every month of the year.

| Payment Cycle | Months Paid |

|---|---|

| Cycle A | January, April, July, October |

| Cycle B | February, May, August, November |

| Cycle C | March, June, September, December |

Hold a few solid companies from each of these three cycles, and you've effectively converted quarterly payments into a monthly income stream — without needing to rely exclusively on monthly-paying stocks, which tend to be a smaller and sometimes riskier pool.

The Metrics That Actually Matter

Chasing the highest dividend yield you can find is one of the most common beginner mistakes. A yield that looks too good to be true usually is — it can signal that a stock price has crashed or that a cut is coming. Instead, weigh these metrics together.

| Metric | What to Look For |

|---|---|

| Dividend Yield | Annual dividend divided by share price. A moderate, sustainable yield generally beats an unusually high one. |

| Payout Ratio | The share of earnings paid out as dividends. A very high ratio leaves little room for error if profits dip. |

| Dividend Growth Streak | How many consecutive years the company has raised its payout — a sign of consistency and discipline. |

| Free Cash Flow | Whether the company actually generates enough cash to comfortably cover its dividend obligations. |

| Debt Levels | Heavily indebted companies are more likely to cut dividends during economic stress. |

A Quick Word on Dividend Aristocrats and Dividend Kings

Two terms come up often once you start researching: Dividend Aristocrats are companies that have increased their dividend for at least 25 consecutive years, while Dividend Kingshave done so for 50 years or more. These lists are a useful starting point for research precisely because that kind of track record filters out companies that can't sustain their payouts through recessions, downturns, and industry shifts. They're not automatically "safe," but the screening criteria alone tends to weed out weaker businesses.

Individual Dividend Stocks vs. Dividend ETFs

One of the first real decisions you'll face is whether to hand-pick individual stocks or buy a fund that holds dozens (or hundreds) of them at once.

- Individual stocks give you full control over which companies you own, and let you build the monthly payment schedule described above with precision. The trade-off is concentration risk — if one company cuts its dividend or struggles, it directly affects your portfolio.

- Dividend ETFs and mutual funds spread your money across many companies automatically, reducing the impact of any single dividend cut. Many also pay out monthly, which simplifies the income-scheduling problem entirely. The trade-off is less control and, usually, a small ongoing management fee.

Many beginners land somewhere in the middle: a core holding of one or two diversified dividend ETFs, supplemented with a handful of individual stocks they've researched and believe in.

The Power of Reinvesting: How DRIP Accelerates Growth

A Dividend Reinvestment Plan, or DRIP, automatically uses your dividend payments to buy more shares of the same stock or fund — often without any additional trading fees. It sounds like a small detail, but the long-term effect is significant.

Each reinvested dividend buys you more shares, which then generate their own dividends next quarter. Over ten, twenty, or thirty years, this compounding effect can meaningfully outpace simply collecting the cash and leaving it idle. Most brokers let you toggle DRIP on or off for each holding, so you can reinvest while building your portfolio and later switch to collecting cash once you actually want the income.

Taxes on Dividend Income

Tax treatment of dividends varies significantly depending on where you live, what type of account holds the investment, and how the dividend is classified. In many countries, dividends held in a standard taxable brokerage account are taxed differently than those held in a tax-advantaged retirement account, and "qualified" dividends are often taxed at a lower rate than ordinary income.

Because rules differ so much by jurisdiction and change over time, this article can't substitute for personalized guidance. It's worth checking your local tax authority's current guidance or speaking with a qualified tax professional before assuming how your dividend income will be taxed.

Common Mistakes Beginners Make

- Chasing the highest yield. An unusually high yield is often a warning sign, not a bargain.

- Ignoring diversification. Concentrating in one sector (utilities or REITs, for example) leaves your income exposed to sector-specific downturns.

- Overlooking the payout ratio. A company paying out nearly all of its earnings has little cushion if business slows down.

- Expecting overnight income. Meaningful monthly income usually takes years of consistent contributions and reinvestment to build.

- Forgetting about fees and taxes. These quietly erode returns if left unmanaged.

How to Start Dividend Investing: A Step-by-Step Overview

- Open a brokerage account that supports fractional shares and, ideally, commission-free trades.

- Decide on an account type — a taxable account, or a tax-advantaged retirement account if one is available and suits your goals.

- Set a monthly contribution you can realistically sustain, even if it's modest at first.

- Research a handful of candidates using the metrics above rather than yield alone.

- Stagger your purchases across different payment cycles if a monthly cash flow is your goal.

- Turn on DRIP while you're still building the portfolio, then reassess once you want the cash.

- Review annually — check payout ratios and dividend growth to catch warning signs early.

Risks Worth Understanding

Dividend investing isn't risk-free, and treating it as a guaranteed paycheck is a mistake. Share prices can still fall. Companies can and do cut or suspend dividends during recessions or industry disruption. Concentrating too heavily in high-yield sectors can leave a portfolio more exposed than it appears. As with any investment strategy, diversification, ongoing research, and a long time horizon matter far more than any single stock pick.

Frequently Asked Questions

How much money do I need to start dividend investing?

Thanks to fractional shares and commission-free brokers, you can start with as little as $50 to $100. Consistency over time matters more than the size of your first deposit.

Can dividend investing really replace a salary?

It can, but it usually takes many years of consistent investing and reinvesting to build a portfolio large enough to cover living expenses. Most people use dividend income to supplement other income first, then scale it up over a decade or more.

Are dividend stocks safer than growth stocks?

Not automatically. Dividend-paying companies tend to be more mature and stable, which can mean lower volatility, but any stock can lose value and any company can cut its dividend. Diversification and research still matter.

Do dividends get taxed?

In most countries, yes. Tax treatment depends on where you live, the type of account you use, and whether the dividend is classified as qualified or ordinary. Check local tax rules or speak with a tax professional for guidance specific to your situation.

The Bottom Line

Dividend investing rewards patience more than timing. The path is straightforward even if it isn't fast: pick sound, financially healthy companies or funds, stagger payment schedules if monthly income is your goal, reinvest while you're building, and let compounding do the heavy lifting over years, not weeks. Start small, stay consistent, and revisit your holdings periodically — the snowball effect does the rest.

This article is for educational purposes only and does not constitute financial or tax advice. Consider speaking with a licensed financial advisor before making investment decisions.